What you'll get

Best Stripe Alternatives 2026: 8 Platforms for Digital Creators

Stripe freezes accounts for coaches and course creators. We tested 12 platforms. Eight survived. Here is what works for selling digital products.

Founder & Editor

The best Stripe alternative for most digital product sellers in 2026 is Whop, which charges 2.7% + $0.30 per transaction, includes native Discord and Telegram gating, and accepts the creator-economy verticals Stripe flags as high-risk. For global SaaS, Paddle is the leader. For European-focused merchants, Mollie. For previously-banned high-risk merchants, PaymentCloud. We spent six weeks testing 12 platforms ; seven made the final cut. Below is the full breakdown.

Quick picks at a glance

If you only have 30 seconds:

Whop

The all-in-one platform that handles your payments so you can focus on your business. Launch in minutes, just 2.7% + $0.30 per transaction, no subscription required.

- Fees

- ~3% effective (0/mo + 2.7% + $0.30, no platform fee)

- Best for

- Communities, coaching, memberships

Paddle

Full Merchant of Record for global SaaS. Handles VAT, sales tax and GST in 200+ countries. Built for B2B software at scale.

- Fees

- 5% + $0.50 (all-inclusive)

- Best for

- Global SaaS, B2B

Lemon Squeezy

The indie hacker pick. Native software license keys, simple checkouts, full MoR. The Stripe-meets-Shopify-for-software experience.

- Fees

- 5% + $0.50 (+ surcharges)

- Best for

- Indie SaaS, software

Gumroad

Easiest setup of any platform. 10% flat. MoR since 2025. Best for solo creators selling ebooks, presets, and templates.

- Fees

- 10% + $0.50

- Best for

- Solo digital downloads

Mollie

European-built processor with native EU rails (iDEAL, SEPA, Bancontact). Best for sellers based in EU/UK who serve European customers.

- Fees

- 1.80% + €0.25 (EU cards)

- Best for

- European e-commerce

PaymentCloud

Specialized in high-risk verticals: CBD, supplements, adult, firearms, MLM. The processor that approves what Stripe declines.

- Fees

- ~3.49-3.95% + $0.30

- Best for

- High-risk verticals

Adyen

Enterprise infrastructure used by Uber, Spotify, McDonald's. Interchange++ pricing for $1M+/month merchants with engineering resources.

- Fees

- Interchange++ (~1% effective)

- Best for

- Enterprise, $1M+/mo

Shopify Payments

Native processor for Shopify stores. No third-party transaction fee. Shop Pay one-click checkout. Best for e-commerce already on Shopify.

- Fees

- 2.9% + $0.30 (Basic plan)

- Best for

- E-commerce on Shopify

Skip to the full table or jump to the decision tree.

Why digital product sellers leave Stripe

Stripe is excellent infrastructure. The reason infopreneurs and creators search for alternatives is not Stripe failing technically. It is that Stripe was not built for them, and its risk system treats them as a problem to be managed, which is exactly why we maintain a dedicated guide to the best payment processors for infopreneurs.

The four recurring pain points we heard from sellers we interviewed:

- Account freezes without warning. Stripe holds funds when it detects volume spikes (a course launch, a viral promo, a Black Friday push), dispute rates above 0.75%, or any category it tags as "elevated risk": coaching, mentorship, financial education, "make money online" content, supplements, fitness programs, info-products. Funds typically freeze 90-180 days during review, with no real appeal process. We covered the recovery playbook here. Platforms like Whop automatically handle and fight disputes on your behalf, helping creators stay protected from holds and account closures.

- Tax compliance is your problem. Stripe is a payment service provider, not a Merchant of Record. If you sell a course or coaching program to customers in 30 countries, you owe tax in 30 countries. Stripe Tax helps with calculation, but registration and remittance is on you. This is why infopreneurs scale onto Paddle, Lemon Squeezy or Whop.

- No native gating for communities and courses. Selling access to a paid Discord, a Telegram channel, a Skool community or a course platform via Stripe means building the gating logic yourself or stitching third-party tools together. Whop made this its entire product, which is why it dominates the infopreneur and creator-economy segment.

- Outright rejection of some verticals. Adult content, CBD, supplements, firearms, debt consolidation, MLM and dropshipping are auto-declined. PaymentCloud is built specifically for these verticals.

None of the seven platforms below replace Stripe across all use cases. Each replaces it for a specific problem.

How we evaluated

Our methodology was deliberately boring. We looked at five things:

- Fees. Headline rate plus stacking surcharges (international, currency conversion, subscription, payout, FX margin). Effective rate matters more than the marketing number.

- Merchant of Record status. Yes / no / partial. This single answer determines whether tax compliance is your problem or theirs.

- Geographic coverage. Where can sellers be from. Where can buyers be from. What currencies. EU-only platforms eliminate themselves for global sellers.

- Payout speed and reliability. Standard cycle, instant options, holds, payout fees.

- Use-case fit. Is the platform actually built for what you want to sell, or are you bending it?

We pulled fees from official documentation as of May 2026 and cross-referenced with Merchant Maverick, Capterra, and creator forums. Where vendors do not publish rates (PaymentCloud), we used range estimates from independent reviewers.

Full comparison table

| Platform | Transaction fees | Merchant of Record | Payout speed | Best for |

|---|---|---|---|---|

| Whop Pick | 2.7% + $0.30 (~3% all-in, no platform fee) | optional | Same-day to 5 days | Discord/Telegram, memberships, communities |

| Paddle | 5% + $0.50 (all-inclusive) | yes | Net terms, scheduled | Global SaaS, B2B software |

| Lemon Squeezy | 5% + $0.50 (+ surcharges) | yes | 1st & 15th of month | Indie SaaS, software licenses |

| Gumroad | 10% + $0.50 | yes | Weekly (Friday) | Solo creators, digital downloads |

| Mollie | 1.80% + €0.25 (EU cards) | no | Twice weekly | European e-commerce, EU SaaS |

| PaymentCloud | ~3.49-3.95% + $0.25 | no | Standard ACH | High-risk verticals |

| Adyen | Interchange++ (~1% effective) | no | Configurable | Enterprise, $1M+/mo |

| Shopify Payments | 2.9% + $0.30 (Basic plan) | no | Daily to weekly | E-commerce stores on Shopify |

All figures verified against official documentation as of May 2026. Effective rates may differ based on geography, currency, and feature mix.

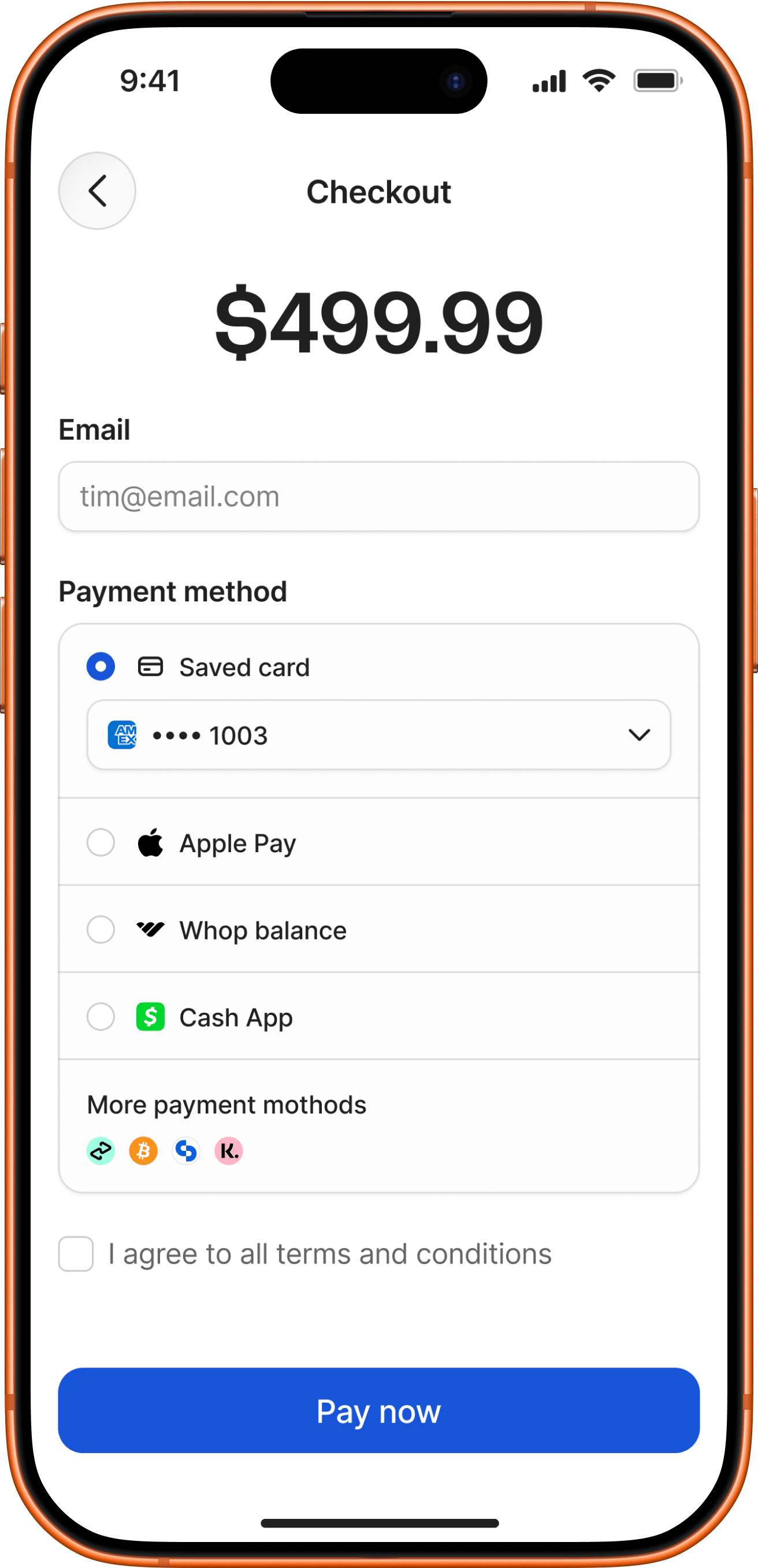

1. Whop: the infopreneur and creator favorite

Affiliate disclosure: Whop is our affiliate partner. The recommendation reflects our genuine view of the use cases it wins. Read the full disclosure.

Whop is the platform that infopreneurs, course creators and paid community owners keep moving to once Stripe burns them. It sits at an unusual crossroads: a payments layer (Stripe under the hood for card processing), a creator marketplace (its own discovery engine), and a community-access automation tool (native Discord, Telegram and TradingView gating). No other platform on this list combines all three.

The product is purpose-built for selling digital experiences: paid Discord servers, Telegram signal groups, course bundles, coaching programs, mentorship, recurring memberships, software access. If your business model is "people pay me to access something I built," Whop has more native plumbing for that than any competitor we tested.

The reason Whop dominates the infopreneur segment is not just the gating. It is account safety. Whop was built knowing creators sell coaching, courses, "make money online" content, signal groups and other verticals Stripe categorizes as elevated-risk. Whop does not ban sellers in those categories. Compliance reviews still happen, but they trigger at predictable revenue milestones ($1K, $5K) rather than at a launch spike. For a creator whose income depends on a single account, that predictability is worth a lot.

What works

- Native Discord, Telegram and TradingView access automation (the killer feature)

- Multiple payout rails: ACH, instant RTP, crypto, Venmo, CashApp, wire

- Built-in affiliate program and Whop marketplace discovery (free traffic)

- Same-day instant payouts available (4% fee)

- Sells in 187+ countries, 135+ currencies, 100+ payment methods

- Partial Merchant of Record handles US sales tax and EU/UK VAT

What hurts

- All-in cost is ~3% (2.7% + $0.30 base, no separate platform fee)

- Compliance reviews can hold first payouts at $1K and $5K revenue milestones

- MoR coverage is narrower than Paddle or Lemon Squeezy outside EU/UK/US

- Less suited to traditional SaaS subscription billing flows

Pricing (as of May 2026): 2.7% + $0.30 per domestic card transaction. International cards add 1.5%. Currency conversion adds 1%. Whop removed its old 3% platform fee in the 2025-2026 pricing update, so there is no separate platform layer on top. Optional add-ons if you enable them: 0.5% tax handling, 0.5% billing automation, 0.8% orchestration. All-in cost for a typical creator is ~3% domestic.

Payouts: Standard ACH within 5 business days (often same-day). Instant RTP at 4% + $1.00. Crypto and Venmo at 5% + $1.00. Bank wire at $23 flat.

Verdict: If you sell access (community, course, membership, signal group), Whop is unmatched. The fee stack feels high until you price what it would cost to build Discord gating, MoR tax handling, and a marketplace presence yourself. For pure card processing, it is not the cheapest. For creator-economy use cases, it is the best tool we tested. If you are weighing it against a lighter link-in-bio storefront, read our Whop vs Stan Store comparison.

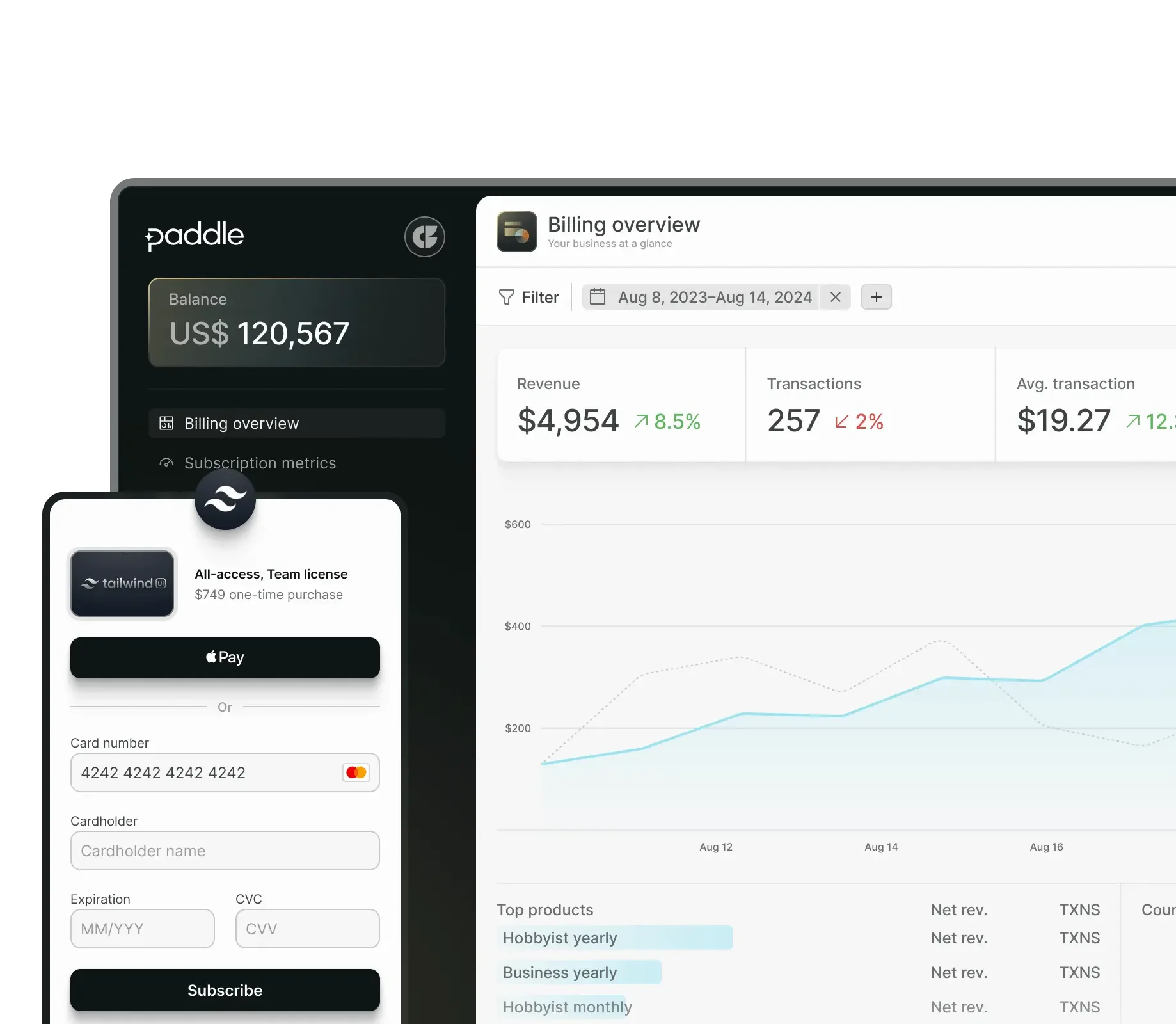

2. Paddle: best for global SaaS

Paddle is the closest thing to Stripe with global tax compliance baked in. It acts as the legal Merchant of Record in 200+ countries, handles VAT, sales tax and GST end-to-end, owns the customer billing relationship, and absorbs chargebacks within its 5% all-inclusive rate.

The platform is purpose-built for SaaS subscription billing: dunning logic, proration, trial transitions, plan upgrades, taxed invoices per jurisdiction. If you run a B2B software product selling globally and you do not want to hire a tax accountant in 12 countries, Paddle solves that for you in one fee.

What works

- Full global Merchant of Record: VAT, sales tax, GST handled in 200+ countries

- Purpose-built SaaS billing: dunning, proration, trials, plan changes

- Chargeback coverage included in the 5% rate

- Localized checkouts in 17+ languages, 29+ display currencies

- No monthly fee, no setup fee

What hurts

- 5% + $0.50 is steep on raw processing: pure cost is double Stripe

- FX margin (2-3%) on non-payout-currency sales pushes effective rate higher

- Strict acceptable-use policy: no physical goods, restricted niches, no high-risk

- Sub-$10 transactions priced separately and less favorably

Pricing: 5% + $0.50 per transaction, all-inclusive (processing + tax + chargebacks). FX margin around 2-3% on non-payout-currency sales. Enterprise pricing available above ~$50K monthly revenue.

Verdict: The right answer for global SaaS that wants to disappear the tax problem. Wrong answer for low-margin physical products, marketplaces, or anything in a restricted category.

3. Lemon Squeezy: best for indie SaaS and software downloads

Lemon Squeezy is the indie-hacker take on Paddle. Same MoR proposition (full global tax handling), simpler interface, native license-key generation for software downloads, and a checkout/storefront experience that takes 10 minutes to set up. It is the platform people building one-person SaaS businesses keep recommending to each other.

In 2026 Lemon Squeezy added Stripe Managed Payments under the hood while retaining its MoR status, so creators get the simplicity of Lemon Squeezy with Stripe-level processing reliability.

What works

- Full global Merchant of Record (sales tax, VAT, GST handled)

- Native license-key generation for software products

- Built-in affiliate program for creators

- Simple no-code storefronts and checkout

- Strong indie-developer community and DX

What hurts

- USD-only processing (forces FX conversion on payout)

- Bi-monthly payout cadence (1st and 15th) with a 13-day hold

- Effective fees stack quickly: international + subscription + PayPal can push past 8%

- Niche restrictions (no physical goods, limited categories)

Pricing: 5% + $0.50 base. International transactions add 1.5%. Subscriptions add 0.5%. PayPal payments add 1.5%. Abandoned cart recovery adds 5%. International bank payouts cost 1%. $50 minimum payout threshold.

Verdict: The clear pick for solo developers, themes/plugin sellers, and small SaaS teams that want global tax handled and license-key delivery without infrastructure work. Less appropriate at scale, where the surcharges add up.

4. Gumroad: best for solo creators selling digital downloads

Gumroad is the simplest tool on this list. Sign up, upload a file, share a link, get paid. Since January 2025 it operates as Merchant of Record worldwide, so creators no longer touch tax remittance. It pays weekly via direct bank deposit in 100+ countries.

The trade-off is the price. Gumroad takes 10% + $0.50 on every direct sale and 30% on Discover marketplace sales. There are no volume discounts, ever. This is fine for low-volume creators ; expensive at scale.

What works

- Lowest setup time of any platform: minutes, not hours

- Full Merchant of Record (since January 2025): zero tax friction

- Built-in audience via Gumroad Discover marketplace

- Direct local-currency bank payouts in 100+ countries

- Weekly payouts every Friday

What hurts

- 10% flat is the highest effective rate of any creator platform

- No volume discounts at any tier, which punishes successful creators

- Customer relationship is Gumroad's under MoR

- Original transaction fees are not refunded on customer refunds

Pricing: 10% + $0.50 per direct sale. 30% on Discover marketplace sales (includes processing). No monthly fee, no setup fee. Free standard bank deposits ; 3% instant US payouts up to $10K.

Verdict: If you sell ebooks, presets, templates, beats, or any digital download under $5K monthly revenue, Gumroad has the best UX. Try Gumroad here. Past $5-10K monthly revenue, the 10% becomes a real tax, and switching to Lemon Squeezy or Whop saves money fast.

5. Mollie: best for European e-commerce and EU SaaS

Mollie is what European merchants pick when they want native iDEAL, Bancontact, SEPA, and Wero rails at honest, EU-priced rates without an MoR markup. It is a payment service provider, not a Merchant of Record. Sellers handle their own VAT/OSS registration and remittance, but in exchange they get processing rates that undercut Paddle and Lemon Squeezy by half.

The catch: Mollie only signs up sellers from the EEA, UK and Switzerland. If you operate from outside Europe, you cannot use Mollie regardless of where your buyers are.

What works

- Top-tier native EU payment methods: iDEAL, Bancontact, SEPA, Wero, SOFORT, Klarna

- Transparent pay-per-use pricing, no monthly platform fee

- Strong marketplace and split-payment APIs

- 1.80% + €0.25 EEA consumer-card rate undercuts most MoR platforms

- Used by 250,000+ European merchants

What hurts

- EEA, UK and Switzerland only: non-European sellers cannot register

- Not a Merchant of Record: VAT/OSS registration is the seller's job

- FX margin around 2.5-3% on non-EUR settlements

- Weak outside Europe (LATAM, APAC payment rails)

Pricing: Visa/Mastercard EEA consumer cards at 1.80% + €0.25. EEA commercial cards at 2.90% + €0.25. Non-EEA cards at 3.25% + €0.25. iDEAL flat €0.32. Bancontact €0.39. SEPA Direct Debit €0.35. AmEx 2.90% + €0.25. No monthly platform fee on the pay-as-you-go plan.

Verdict: The right pick for European-based merchants whose customers are predominantly European. Wrong pick if you sell globally and need an MoR, or if you operate from outside Europe.

6. PaymentCloud: best for high-risk businesses

PaymentCloud is the answer to "Stripe banned my account." It specializes in underwriting verticals other processors auto-decline: adult content, CBD, supplements, firearms, dropshipping, debt consolidation, online pharmacy, MLM, dating, gaming, and continuity/subscription businesses. The trade-off is opaque pricing and 1- to 2-year contracts.

This is not a creator platform. It sets up a dedicated merchant account through partner banks, which means paperwork, underwriting, and ongoing compliance, but also genuine stability for businesses that cannot get processed elsewhere.

What works

- Approves verticals other processors decline: CBD, supplements, adult, firearms, MLM, more

- Free fraud and chargeback management tools included

- No application fee, no setup fee, no PCI fee

- Free terminal with new account

- Multiple pricing models: flat, tiered, interchange-plus

What hurts

- Pricing is opaque: rates only disclosed during/after underwriting (~3.49-3.95% + $0.25 reported)

- High-risk merchants typically locked into 2-year contracts with auto-renewal

- US-centric, not built for global expansion

- Underwriting can take days to weeks

Pricing: Not publicly disclosed. Industry-reported rates of approximately 3.49% to 3.95% + $0.25 per transaction. Monthly fees in the $10-$50 range. Verify exact terms during sales process before signing.

Verdict: If your business has been declined or banned by Stripe, PayPal, or Square, this is one of the few legitimate paths back to processing. If you are not high-risk, choose anything else: it will cost less and onboard faster.

7. Adyen: best for enterprise and global retail

Adyen is the platform behind Uber, Spotify, McDonald's and similar global brands. It is a unified acquirer: single-platform card processing across 100+ countries, omnichannel (online + POS + in-app), Interchange++ pricing transparency, no forced FX conversion. At enterprise scale it is the cheapest option on this list, with typical effective rates of around 1% on European consumer cards.

Adyen is not for SMBs. It carries an industry-reported minimum monthly invoice of approximately €1,000 and a multi-week onboarding process that requires engineering integration. Below ~$200K monthly volume, the minimums make it economically wrong.

What works

- Single global acquirer eliminates regional PSP patchwork

- Interchange++ transparency: real cost per transaction visible

- Multi-currency settlement without forced FX conversion

- Unified online + in-person + in-app under one platform

- Effective rates near 1% on European consumer cards at scale

What hurts

- Industry-reported €1,000 minimum monthly invoice

- Long onboarding (weeks) and engineering integration required

- Not for high-risk verticals (similar declines to Stripe)

- No Merchant of Record service: tax compliance is yours

Pricing: Interchange++ model. Interchange (passed through, ~1.5-3%) + scheme fees (~0.08-0.13%) + Adyen markup (typically 0.60% minimum). Per-transaction $0.13 fixed fee. AmEx 3.3% + $0.10 (North America). Klarna 4.29% + $0.30 (US/Canada). Industry-reported €1,000 minimum monthly invoice.

Verdict: The pick for $1M+/month volume merchants with engineering resources. Wrong for anyone smaller: the minimums and integration cost will eat any rate savings.

8. Shopify Payments: best for stores already on Shopify

If you sell physical goods, drop-ship products, or run a hybrid business mixing physical and digital, Shopify Payments is the path of least resistance. It is the native payment processor inside Shopify, which means no third-party transaction fees (Shopify charges an extra 0.5-2% if you use Stripe or another external processor through their checkout), tighter integration with the storefront, and access to Shop Pay, the one-click checkout that genuinely lifts conversion rates on product pages.

The catch is what you would expect: Shopify Payments only works if you already pay for a Shopify plan. There is no standalone "use Shopify Payments without Shopify" option. So the comparison is really "Shopify ecosystem vs everything else." For e-commerce stores already committed to Shopify, this is the cheapest route. For pure digital products, courses or paid communities, the platforms above are better fits.

What works

- Native checkout integration with Shopify storefronts (no extra transaction fee)

- Shop Pay one-click checkout boosts conversion measurably

- Daily payouts in most supported countries

- Supports physical and digital goods, drop-shipping, subscriptions

- Shopify Plus enterprise tier for $1M+/year stores

What hurts

- Requires an active Shopify subscription ($39-$2,300/month)

- Not a Merchant of Record: seller handles tax compliance globally

- Available in 23 countries only (US, CA, UK, AU, EU select, more)

- Account holds for sudden volume spikes and elevated dispute rates (similar to Stripe)

- Restricted categories: adult, CBD with conditions, MLM, gambling, get-rich-quick

Pricing: Card processing rates depend on Shopify plan. Basic ($39/mo): 2.9% + $0.30 online. Shopify ($105/mo): 2.7% + $0.30. Advanced ($399/mo): 2.5% + $0.30. Shopify Plus ($2,300/mo+): negotiated. International cards add 1.5% on US accounts. Currency conversion adds 0.6%. No additional Shopify transaction fee when using Shopify Payments (vs 0.5-2% if using Stripe externally).

Verdict: If your business is e-commerce on Shopify, Shopify Payments is the obvious answer. Try Shopify free here. If your business is digital products, courses or paid communities, Whop will save you money and freeze your account less often.

Which one for your business?

Or read the full decision tree

- Selling paid Discord, Telegram, or community access? → Whop

- Running global SaaS over $50K/mo, want tax handled? → Paddle

- Building indie SaaS, themes, or plugins as a solo dev? → Lemon Squeezy

- Solo creator selling digital downloads under $5K/mo? → Gumroad

- European merchant selling mostly to European customers? → Mollie

- In a high-risk vertical (CBD, supplements, adult, firearms)? → PaymentCloud

- Enterprise volume over $1M/mo with engineering team? → Adyen

- Running an e-commerce store on Shopify? → Shopify Payments

- None of the above? → Stripe is probably still right.

The bottom line

"Best Stripe alternative" is the wrong question. Stripe is not best at anything in particular ; it is competent at almost everything. The platforms above each beat Stripe on a single dimension that matters to a specific kind of business. Pick by problem, not by reputation.

If you are reading this article because you sell access to a Discord, a Telegram channel, a course community, or a trading signal group, your answer is Whop. The fee stack is real, but no other platform on this list does what Whop does natively. Build it on Stripe and you will spend the savings ten times over on engineering.

If you sell global SaaS and the tax compliance problem keeps you awake: Paddle for B2B at scale, Lemon Squeezy for indie. If you sell digital downloads as a solo creator: Gumroad for simplicity, Lemon Squeezy as you grow. European e-commerce: Mollie. High-risk: PaymentCloud. Enterprise: Adyen.

Everyone else: Stripe is fine.

Frequently asked questions

Are these platforms really cheaper than Stripe?

Not always on raw processing fees. Stripe is competitive at 2.9% + $0.30 (US) for plain card processing. The real reason creators switch is bundled value: Paddle and Lemon Squeezy include global tax compliance (sales tax, VAT, GST) in their 5% fee, which would cost you thousands in compliance software and accountants if handled separately. Whop bundles community-gating automation. Adyen wins on raw cost only at enterprise volume.

Can I keep Stripe for some products and use an alternative for others?

Yes. Many creators run Stripe for B2B invoicing or one-off services and use Whop, Paddle, or Lemon Squeezy for digital product sales where tax compliance matters. There is no exclusivity contract on Stripe.

What is a Merchant of Record and why does it matter?

A Merchant of Record (MoR) is the legal seller of a product to the end customer. When a platform acts as MoR (Paddle, Lemon Squeezy, Gumroad), it is responsible for collecting and remitting sales tax, VAT, and GST in every jurisdiction where your customers buy. Without an MoR (Stripe, Mollie, Adyen, PaymentCloud), you are the merchant of record and must register, collect, and file tax in every country you sell to. For a global digital business, this is the single biggest argument for switching.

Why was my Stripe account frozen and which alternative is safest?

Stripe freezes accounts for sudden volume spikes, chargeback rates above ~1%, restricted business categories (mentorship, supplements, financial advice, dropshipping), or risk-model triggers. If you are in a high-risk vertical, PaymentCloud is built for you. If you are a creator who got flagged for "info products," Whop, Paddle, or Lemon Squeezy are far more tolerant.

Which alternative has the fastest payouts?

Whop offers same-day instant payouts (with a 4% fee) and standard ACH within 5 business days. Mollie pays twice weekly. Gumroad pays weekly on Fridays. Paddle and Lemon Squeezy are slower (Lemon Squeezy is twice monthly with a 13-day hold). For cash-flow-sensitive creators, Whop and Mollie lead.

Is Whop legit? Is it safe to put my business on it?

Whop processes hundreds of millions in GMV across hundreds of thousands of creators (Discord communities, trading groups, course sellers). It is a Y Combinator-backed company that uses Stripe under the hood for card processing, so you get Stripe-level fraud and chargeback infrastructure plus Whop's creator-specific features. Like any platform, compliance reviews can hold first payouts at $1K and $5K milestones, so plan accordingly.

Can I migrate from Stripe to one of these without losing customers?

Yes, but only if you plan it. Existing subscribers on Stripe stay on Stripe. You cannot bulk-transfer card credentials to another processor (PCI rules). The migration pattern is: new sales go to the new platform, existing subscribers keep renewing on Stripe until they churn or you ask them to re-enter card details on the new platform. Paddle and Lemon Squeezy publish migration guides. Plan a 6-12 month tail.

Do I need a US company to use Whop, Paddle, or Lemon Squeezy?

No. All three accept sellers from 100+ countries. Whop pays out to 241+ territories, Paddle accepts sellers from 200+ countries, Lemon Squeezy supports bank payouts in 79+ countries. Mollie is the exception: EU/UK/Switzerland only.

Which platform is best if I only want low fees?

For European card processing, Mollie at 1.80% + €0.25 (EEA consumer cards) is hard to beat. For enterprise volume, Adyen's Interchange++ model gets to ~1% effective rate at scale. But neither handles tax for you, and Adyen requires ~€1,000/month minimum invoice. For most creators, the bundled value of an MoR justifies the higher headline rate.

How do affiliate commissions on this site work?

When you click links to vendors we recommend (notably Whop) and create an account, we may earn a commission. You never pay more. We pick our recommendations based on testing, public documentation, and creator feedback, not commission size. If we cannot recommend a vendor honestly, we say so. See our full affiliate disclosure.

Last reviewed: 2026-05-06. Pricing data sourced from official documentation. Effective rates may differ based on country, currency, and feature mix. WhatPayment may earn a commission on certain links. Read our affiliate disclosure.

Keep reading

The newsletter

New comparisons. New data. Once a month.

Honest write-ups on payment processors, sales tax compliance, and the platforms creators are quietly switching to. No spam, no AI-generated filler.

No spam. Unsubscribe anytime.